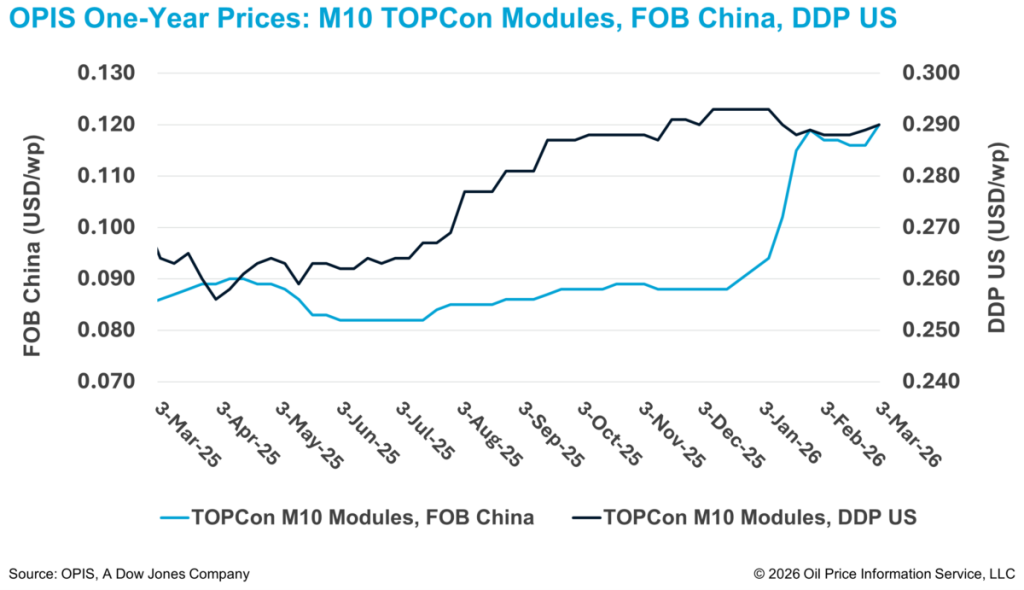

Free-On-Board (FOB) China TOPCon modules rose this week supported by firmer indications for April loading cargoes. Sources from top-tier producers said most March shipments have already been sold out, shifting price discussions toward April and broader Q2 deliveries.

The Chinese Module Marker (CMM), the OPIS benchmark assessment for TOPCon modules from China, rose 3.45% to $0.120/W FOB China, according to the OPIS Global Solar Markets Report released on March 3.

However, trading activity for April remains subdued. Manufacturers noted that buyers are largely staying on the sidelines, anticipating softer prices in the weeks ahead. Many are reluctant to confirm purchases, expecting prices could weaken in April after the cancellation of the export tax rebate. One international module buyer told OPIS they prefer to delay negotiations and reassess pricing conditions after Q1 2026, citing recent market volatility.

Market participants said the Q2 2026 price outlook remains uncertain. Manufacturers continue adjusting production economics in response to shifting export policies, fluctuating input costs, soft end-user demand and industry directives requiring manufacturers to limit operating rates.

According to the OPIS TOPCon module forward curve, Q2 2026 FOB China cargoes were assessed 0.83% lower at $0.120/W, while Q3 2026 cargoes held steady at $0.122/W.

A top-tier manufacturer noted that silver, which previously accounted for only 3-5% of module costs, has become a significant cost driver due to recent price increases and tight supply. The source added that production limits set by industry regulators have compounded cost pressures, as manufacturers are not allowed to operate at full capacity, keeping fixed costs elevated despite lower utilization rates.

In global markets, the recent US-Israel tensions with Iran have so far had limited direct impact on Chinese solar module and cell trading, sources said. Although several Chinese manufacturers have established or are building production capacity in the region, most projects remain at an early development stage, limiting the sector’s direct exposure.

The conflict has, however, had a more immediate effect on container shipping, the primary transport mode for solar products to the region. Several shipping lines to the Middle East have been suspended alongside rising freight rates, and near-term logistical disruptions could delay raw material deliveries and contribute to price volatility.

Meanwhile, in the U.S., the Department of Commerce last week announced preliminary countervailing duties on solar cells and modules imported from companies in India, Indonesia and Laos, citing subsidy support in those markets. The general subsidy rates were set at 125.87% for India, 85.99% to 143.30% for Indonesia, and 80.67% for Laos.

Indian manufacturers described the preliminary CVD rates as unexpectedly high and requested time to assess the pricing impact. A U.S. distributor source added that the ultimate effect will depend on demand for modules from the affected countries – which is likely to weaken as the investigation proceeds and production shifts to new regions – as well as the average selling prices on which the duties are applied.

According to the same OPIS report, the spot price for Delivered Duty Paid (DDP) U.S. TOPCon modules rated 600 W and above rose 0.35% this week to $0.290/W.

Separately, updated U.S. guidance issued earlier this month on Foreign Entity of Concern (FEOC) rules clarified that upstream inputs – including wafers, ingots and polysilicon – are excluded from the calculation of FEOC-related material assistance costs.

Industry sources said the clarification has reduced the urgency for some Chinese manufacturers that had been evaluating overseas production options ahead of China’s planned removal of the 9% export tax rebate for wafer exports in April. The policy change is expected to raise export costs for Chinese wafer producers, but sources said the revised U.S. guidance has led some companies to reassess whether overseas leasing or manufacturing arrangements remain economically justified.